1099 Income Mortgage Loans

Are you a diligent individual trying to secure your share of the American dream with a 1099 income? Look nowhere else! You may navigate the world of mortgage loans with simplicity and confidence thanks to the assistance of our experts.

Our customized solutions are made to meet your particular financial circumstances, whether you’re interested in an FHA loan, a VA loan, or a conventional loan. We acknowledge that your 1099 income might not conform to the norm, but that doesn’t mean you should pass up on the chance to buy a property.

You can easily attain your homeownership goals with our 1099 income mortgage alternatives. Allow us to assist you so the process goes quickly and without incident. Your dream home is within your grasp; begin your quest with us today!

1099 Income Loan

Credit scores starting at 640

Up to 90% LTV, No MI

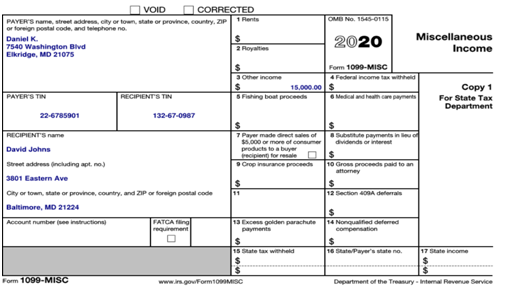

Our 1099 mortgage for self-employed is an income loan option for borrowers who are 1099 earners not able to qualify for a full doc mortgage loan. Tax write-offs make verifying income difficult for self-employed people. This program allows you to use 1099s for the last 2 years in lieu of tax returns

Self-Employed

- Max LTV 90% with 700 score

- Max LTV 80% with 640 score

- Loans up to $3 million, Minimum loan of $150,000

- No tax returns are required

- Most recent one or two years 1099 plus year to date earning statement allowed

- Year to date earnings are verified from earning statement, paystubs, or bank statements

- 1099s must be from a single employer

- Borrower must be self-employed working for the same employer for two years

- Owner-occupied, 2nd homes, and non-owner occupied

- Purchase and cash-out or rate-term refinance

- 4 years seasoning for foreclosure, short sale, bankruptcy or deed-in-lieu

The qualifications for a bank statement loan may vary by lender. But in general, a borrower is required to have at least two years of self-employed income and business experience. Once a lender has determined income, they will decide the maximum loan amount allowed. This is based on the borrower’s debt-to-income ratio, a percentage of the monthly income that goes towards paying any debt they may have, including a mortgage.

Our lenders requires a minimum of two years of self-employment, 12 months of consecutive bank statements from the same account, and the borrower must have a 45% maximum debt-to-income ratio. The maximum loan amount is $1,000,000.

Types of Bank Statement Mortgage Loans in Florida

We currently offer two 1099 mortgage for self-employed borrowers:

- Personal Bank Statements: Qualify on 12 or 24 months bank statements. We count 100 percent of deposits as income.

- Business Bank Statements: Qualify on 12 or 24 months bank statements. We count 50 percent of the deposits as income.